Eleven years ago, I needed a new bike. At the time, I rode a lot. I was in a big group of relatively competitive riders, and we’d often put hundreds of miles on our bikes each week. I agonized over what bike to buy, but I kept coming back to one made by a company called Moots, a Colorado company that builds titanium road and mountain bikes by hand.

The father of a good friend of mine had a Moots bike when I was growing up, and it made me salivate. The problem was, they were really expensive. Like, “far more money than I ever considered spending on a bike” expensive. Maybe $5,000 or so back then.

But the more I looked into it, the more I was convinced I had to have this bike. After putting myself through the painful process of shopping around, comparing prices, and looking at models that I didn’t really want, I pulled the trigger.

Following weeks of buyer’s remorse that more closely resembled terror, I came to realize something that is going to sound crazy. Buying this incredibly expensive bike was one of the best financial decisions I’ve ever made. I understand that writing $5,000 and the words “bike” and “smart financial decision” all in the same sentence sounds absurd, but it’s not.

This was a fantastic, rational, smart financial decision. And I know that goes against everything you’ve heard from every personal finance advisor out there. They’re always telling you how to save money, how to reduce expenses, how to buy cheaper. Right? Cheaper, cheaper, cheaper. What I’m saying is, that’s a shortsighted message that we need to change.

Here are the reasons:

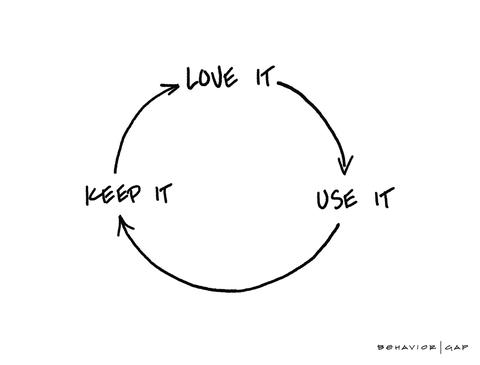

- If you love it, you will keep it; if you keep it, you will use it. I bought a bike I love. You may not like it. That’s fine. If you don’t like it, don’t buy it. But I love it. And since I love it, I’ve kept it for 11 years. And since I’ve kept it for 11 years, I use it all the time.

- It replaces five other bikes. The guys I ride with own plastic bikes (carbon fiber). And they may feel the same way about their bikes as I do about mine, but most of them don’t. Most of them think, “Oh, I’ll just go buy a bike.” A couple years later they buy the newest bike, and a couple years after that they buy the newest bike again. Each time they sell the old one and buy the new one, they lose money. That can be costly. I have changed almost nothing on my road bike in 11 years, and I like it more than when I bought it.

- It will last. Let’s say you follow the standard advice and buy the cheaper bike. We all know what happens with the cheaper bike. It breaks! It wears out, you replace it. And not only does good gear last, but when you buy cheap stuff, you get bored with it. I do not get bored with this bike, and that is why it is saving me money.

- It’s beautiful. That may sound silly, but it’s important. If you’re planning on having something for a long time, you’d better like looking at it. Any time I even consider looking at a new road bike, all I have to do is wash mine and see the beautiful welds, and I fall back in love again. When I’m done and can no longer ride my bike, it will hang above the mantle over my fireplace. That’s how much I love it. It’s a piece of art to me.

- The cognitive benefit. Buying things is agonizing. The cognitive expense of switching, replacing, and constantly thinking about whether you need a new bike or not has a cost associated with it, too. I don’t think about it. I don’t have to think about it. I’ve got the bike I love. Period.

So, I hereby give you permission to consider buying the things you really love — things that may be two, three, or perhaps even four times more expensive than a similar product. I am asking you to consider the possibility that buying stuff you love, regardless of price, may be the best decision you can make.

Consider that if you love it and you’ll use it, you’ll save not only money but retain the cognitive and emotional energy you would have used to replace the thing once a year. You’ve heard of “buy nice, or buy twice,” right? Well this is a derivative of that idea. But don’t just buy nice, buy what you love. If you don’t, you’ll end up hating, and replacing, until you do.

This column, titled The Financial Benefits of Buying What You Love, originally appeared in The New York Times on December 21, 2015.

. . .